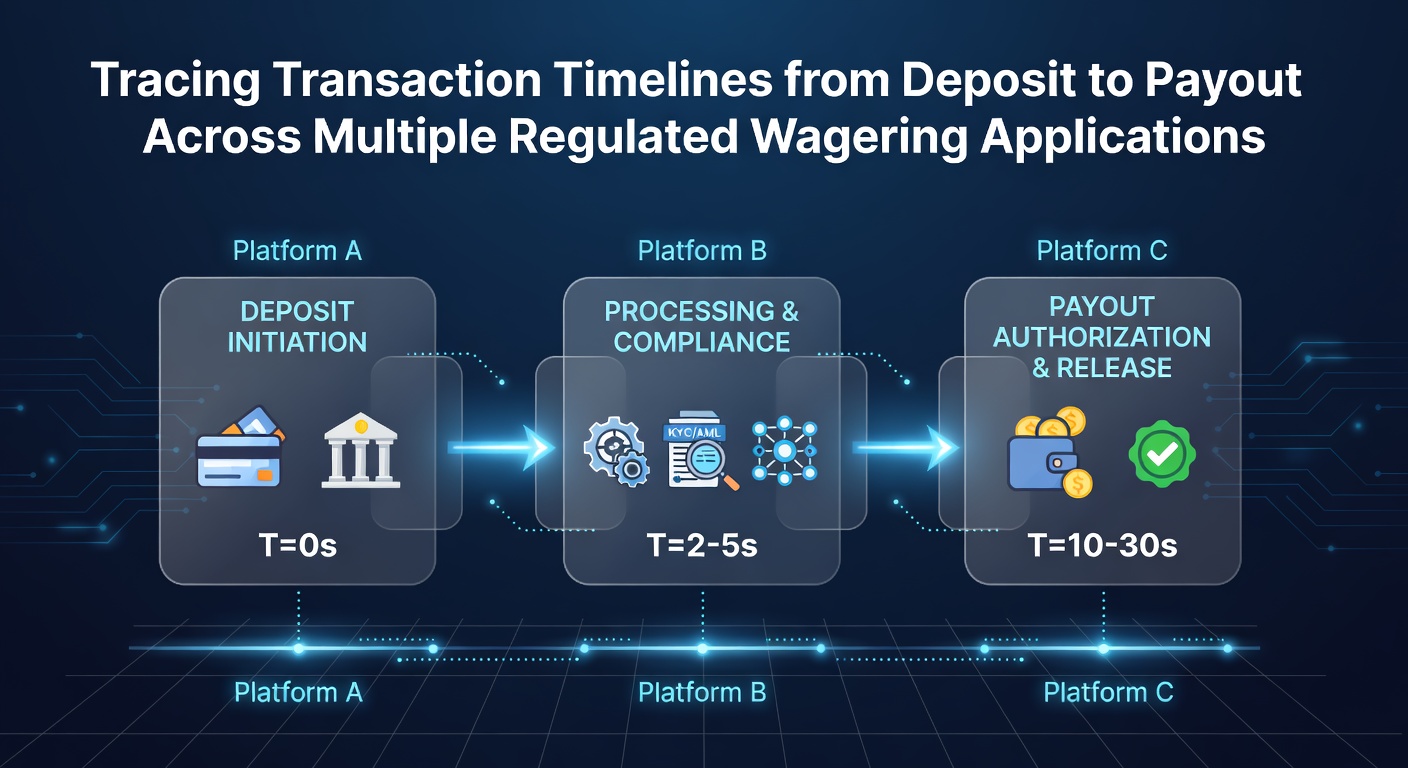

Tracing Transaction Timelines from Deposit to Payout Across Multiple Regulated Wagering Applications

Regulated wagering applications manage deposits and payouts through structured sequences that incorporate payment processor handoffs, identity verification checkpoints, and banking network clearances, all of which create measurable timelines that vary by method and jurisdiction. Operators must route funds through licensed channels while satisfying anti-money laundering protocols, so users encounter predictable delays at each stage rather than instantaneous movement. Data collected through mid-2026 shows these processes have stabilized in most North American and European markets, yet regional differences persist because state and provincial rules dictate how quickly funds can move after initial approval.

Deposit Pathways and Their Processing Windows

Credit and debit card deposits typically clear within seconds once the card network authorizes the transaction, although some platforms hold the funds until a secondary risk screen completes within the first hour. E-wallet transfers from services such as PayPal or Skrill move even faster because the operator already maintains pre-funded accounts, allowing instant credit to the betting balance after the user confirms the amount. Bank transfers and ACH pulls require one to three business days because the originating bank must batch the instruction through the Federal Reserve or equivalent clearing system, and operators in states like Pennsylvania and Michigan add an extra verification layer that can extend the window to five days during high-volume periods. Observers note that as of May 2026 several operators began accepting instant bank transfers through services like Plaid, which reduced average deposit completion times from 48 hours to under four hours for participating users.

Payout Verification and Release Cycles

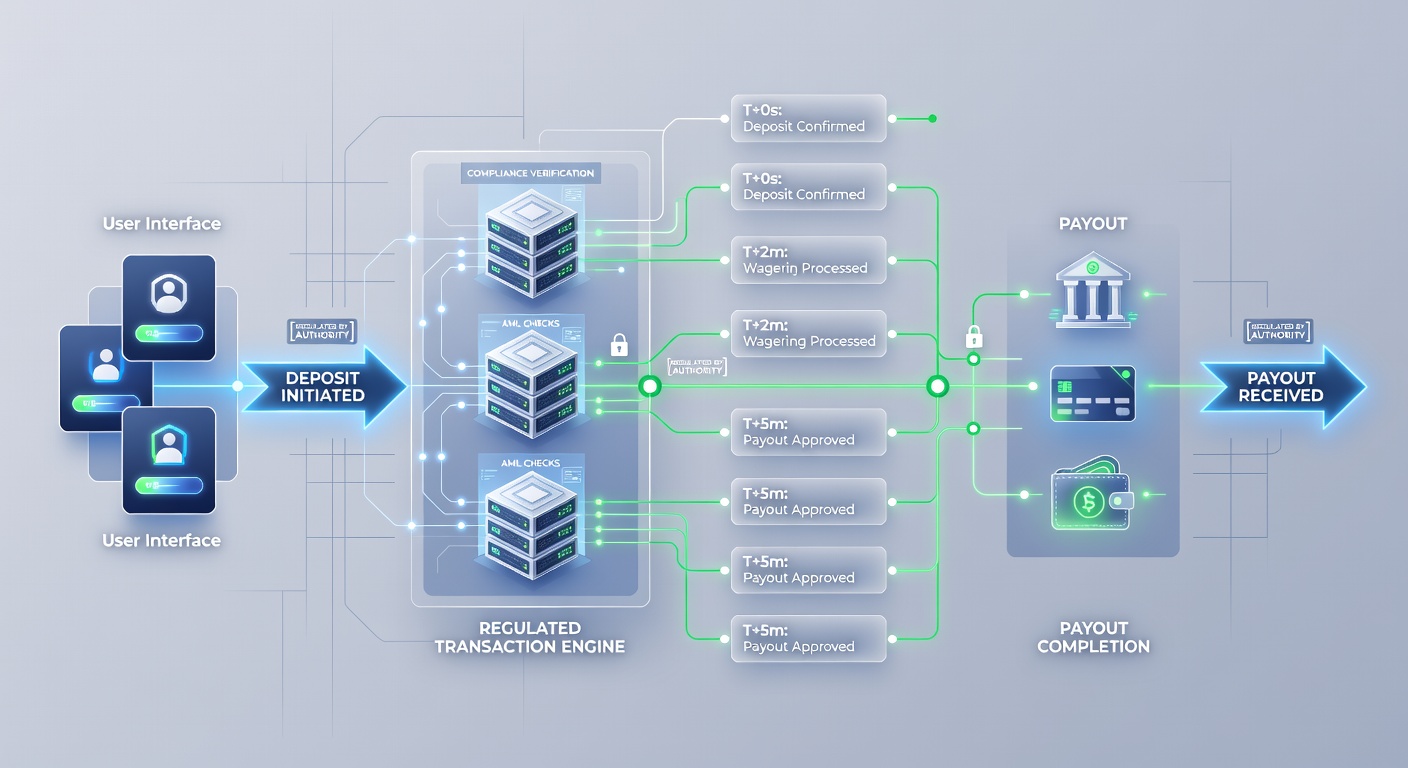

Once a withdrawal request is submitted the platform initiates a compliance review that checks recent betting activity, account age, and any flagged patterns against transaction monitoring software. This review finishes in 24 to 72 hours for most verified accounts, after which the actual fund transfer begins. Credit card withdrawals often return to the original card within three to five business days, while bank wire transfers can take five to seven days because intermediary banks apply their own settlement rules. E-wallet payouts reach the user balance in one to two days once the operator releases the funds, and several major apps now advertise same-day e-wallet processing for users who maintain continuous verification status. Research indicates that average payout approval times across major platforms shortened by roughly 18 percent between January 2025 and May 2026 after operators automated more of their KYC refresh cycles.

Comparative Timelines Across Leading Platforms

Applications operating under multiple state licenses display consistent internal patterns yet still reflect differences driven by local banking partners. One large operator processes card deposits instantly but routes ACH withdrawals through a single processor that clears on Tuesdays and Thursdays only, creating a two-day bottleneck for certain users. Another platform partnered with a Canadian payment rail in early 2026 to offer instant deposits for Ontario users, and those same users now see e-wallet payouts credited within six hours after approval. A third operator maintains separate ledgers for each state license, which means a user verified in New Jersey may wait an additional day compared with the same user verified in New York simply because the New Jersey ledger batches its nightly reconciliation at a different hour. These variations remain visible in transaction logs that regulators require operators to retain for audit purposes.

Regulatory and Compliance Influences on Timing

State gaming commissions and provincial regulators mandate that operators maintain detailed records of every fund movement, and this documentation requirement adds fixed checkpoints that cannot be skipped. The New Jersey Division of Gaming Enforcement, for example, requires daily reconciliation reports that operators must file before they release large payouts, which extends the final release window by one business day for amounts above certain thresholds. In Ontario the iGaming Corporation publishes aggregated performance metrics that show most platforms complete standard payout reviews within 36 hours, yet peak holiday periods push that figure closer to 60 hours because staff volume does not scale linearly. Australian regulators similarly require transaction reports to AUSTRAC within tight windows, forcing operators to front-load compliance checks that lengthen deposit holds for new accounts. Each of these rules creates measurable friction that users experience as extended timelines rather than policy abstractions.

External Payment Network Variables

Beyond operator controls, the underlying payment rails impose their own schedules. Visa and Mastercard networks settle most gaming-related transactions within one business day, yet weekends and holidays pause those clocks because the networks do not process non-essential batches on those days. Traditional ACH transfers clear only on business days, so a withdrawal requested on a Friday afternoon will not begin its journey until the following Monday. Emerging real-time rails such as the RTP network in the United States and the Faster Payments system in other markets bypass some of these calendar restrictions, and operators that adopted them in 2025 reported measurable reductions in user complaints about delayed funds. Observers tracking these changes note that platforms offering multiple rail options now display estimated arrival times at the point of withdrawal so users can select the fastest available route.

Conclusion

Transaction timelines in regulated wagering applications result from the interaction of operator policies, regulatory checkpoints, and payment network schedules, each of which can be quantified and compared across jurisdictions. Users who understand the sequence of verification, batch processing, and settlement days can select methods that align with their timing needs, while operators continue to invest in automation that trims unnecessary delays without compromising compliance standards. The patterns observed through May 2026 indicate that further compression of these timelines will depend on wider adoption of real-time rails and continued harmonization of verification data across state and provincial boundaries.